Today's

Wall Street Journal carries an article by Rebecca Buckman titled

Silicon Valley's Backers Grapple with Era of Diminished Returns. The article catalogs a series of previously well documented and systematic challenges facing the industry:

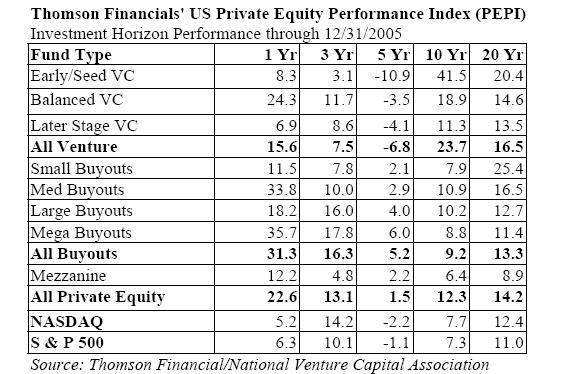

- too many firms (860 US VC firms)

- too much money ($25bn of 2005 LP commitments)

- anemic returns relative to S&P 500 (YTD 3/31/06 returns of 11.7%)

- lack of home run deals (4 of 31 Q2 exits saw 10x+ ROI)

- endowments cutting back VC allocation

- industry leaders, like Paul Ferri, commenting, "I thought by now investors would have figured out that our industry is not an economically viable business model."

To add to the woes, I met yesterday with a very prominent late stage fund who commented that in 70%-80% of their deals, hedge fund money is competing and, more often than not, winning deals at extraordinary valuations.

As with all systemic shocks, the VC industry is adapting and learning to live within the new systemic, rather than cylical, realities of the industry. Clearly, the move to international markets (India and China), new sectors (clean energy), and niche based funds (very early), reflect an implicit realization that the battlefield of opportunity is changing and change will be required for firms to continue to justify their existence and create value.

Brad Feld's blog introduced me to an article by Howard Anderson called

Good-bye to Venture Capital. The article, written by a founder of

Battery Ventures, makes a familiar, yet powerful argument that the venture industry is over-funded, structurally transformed, and doomed to generate returns far lower than what limited partners expect from the asset class and the associated risk profile. As you will read, the article indicts the industry for suffering from too many investors, too much money, and paints a dire picture of the future.

As a recent entrant to the industry, I found the article is powerful food for thought. Is the industry doomed to low double-digit returns? Are there too many of us chasing too few deals funding too many companies selling to customers with finite budgets, abundance of choice, and limited differentiation between vendors? If so, Howard is spot on, returns will fall, capital will leave the industry, and the fees will be significantly lower thereby reducing the number of professional investors in the space.

As an aside, I don't believe that the VC industry is alone is suffering from too much money. The hedge fund industry is simply exploding wrt funds under management, the number of firms, and the number of people entering the space. Capital, itself, appears to be in abundance across the alternative asset management space.

Howard makes one powerful point that resonates with any reader of

Fooled by Randomness. Funds invested in the 1994-19998 time frame did extremely well. The cliche rising tides float all boats comes to mind. At a recent offsite, Eric Schoenberg (HBS prof) reminded us that returns are driven by two key components, systematic returns and idiosyncratic returns (

see CAPM model). Systematic returns are market returns. Idiosyncratic returns, however, are where professional investors earn their stripes - they are returns in excess of the market.

To be a decent investor, one must at least deliver

systematic returns. To be a great investor, one must deliver idiosyncractic returns. In the bubble, random investments looked genius. The systematic returns (returns for the asset category at large) were simply amazing, thereby creating great weath and perhaps reputations for genius that were more due to circumstance and timing than investing prowess.

The questions for us to ponder is what will be the future systemic returns to the venture capital asset class, and has the inflow of money and people into the venture capital industry made it impossible to generate idiosynctratic returns. Are funds' returns systematic (an index of the market) or extroardinary? Will there be a Vanguard-like vc fund that is a low-fee provider of index funds for the private markets!? What is the basis for extraordinary performance over the market index? Is the succes of vc investors and funds due to serendipity or to process?

These are key questions for investors (both general and limited partners). Can one deliver quality returns in an industry full of capital and people chasing "good" ideas?

One key difference between the public equity markets and the venture capital markets is the degree to which information is transparent. The public markets are by regulation open and transparent with

data available to all.The private markets are marked by imperfect information, proprietary insights, and information asymetries. Certain private investors simply enjoy access to information, ideas, and talent that are not generally available to others. For exmaple, certain leading firms leverage the footprint of their portfolio (talent, ideas, reach) to drive insights that lead to investments that others are not in a position to make. An obvious example, is Sequoia Capital's investment in Yahoo! and Google. With a BOD seat at YHOO, Mike Moritz enjoyed acccess to information relative to GOOG's search technology simply not available to others weighing the decision to invest in GOOG, presuming they even had the chance.

The question for venture capitalists may be as simple as, "what do I know that others don't?" With the corallary, yet vital question begging, "will I be smart enough and sufficiently certain of myself to act on such information?" For as Keynes famously once said, "Worldly wisdom teaches that it is better for reputation to fail conventionally than to succeed unconventionally."

If one knows nothing proprietary, has no unique relationships, access to ideas, and information, then life may be very challenging.