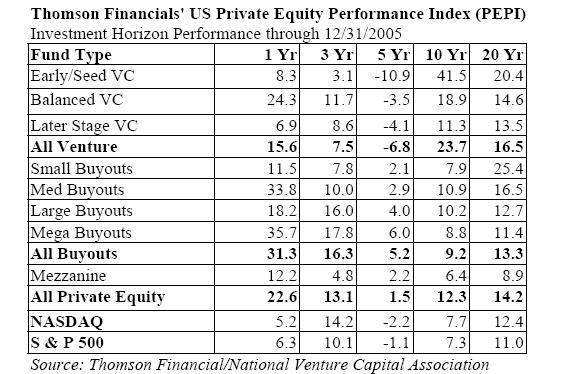

The NVCA and Thomson Financial recently released private equity performance data.

The chart provides a twenty year comparison between the returns to specific private equity strategies, as well as to the NASDAQ and S&P 500.

The private equity returns are net of management fees and carry. 71% of the private equity gains reflect realized returns, while the balance of the total return is calculated by taking the current net asset values of the funds as reported to limited partners.

In the last ten years, limited partners have received distributions totaling $202bn, or an average of $20.3 bn per year, while over the same period limiteds made $829bn in commitments, or an average of $83bn per year.

While the 20 year early stage vs S&P 500 risk premium is only 9.4%, over a 20 year period this represents a 6x difference in total dollars returned.

I am banking on the fact that the ability of top firms to maintain access to non-public information, ideas, entrepreneurs, and information asymmetries will support the continued historical investment performance of early stage venture capital despite the 2x increase in number of VC firms, 1.9x increase in number of VC professionals, 2.5x increase in the amount of VC raised, and 3.2x increase in the average capital under management over the last ten years.

Early stage VC is a tough, tough business. I believe that the best firms demonstrate that a commitment to supporting the entrepreneur, while working to create an unfair advantage with respect to information and access to opportunity supports extraordinary performance relative to the industry at large. It will fascinating to watch if the rolling 20 year returns to early stage venture remain in the 20+% range.

So the returns are interesting by themselves, but not as useful as they would be if they included volatility and correlation data. Could one have done as well on a risk adjusted basis by just building a leveraged NASDAQ index fund?

ReplyDeleteVery, very useful.

ReplyDeleteWould be interesting to know what the distribution of investment returns is across firms. Rumor has it the top 10% of VC firms represent most of the returns.

Two questions that need to be answered before this can be truly credible:

ReplyDelete1. Is this result free of survivor bias?

2. How do the results change on a dollar-weighted basis? Lots of money flowed in at the top, not much money when results would be good in the future. My suspicion is that VC won't look so good on a dollar-weighted basis.

David Merkel