A few weeks ago, I wrote a post on applied interviewing. Mark Tsimelzon, founder and President of Coral8, replied that Coral8 is a strong advocate of structured interviewing and has had tremendous success hiring the best and brightest by a well-defined, consistently applied hiring methodology. Mark kindly offered to serve as this blog's first guest writer and the post below is a wonderful "how to" structured interviewing guide. Thanks to Mark!

A Practical Guide to Structured Interviewing ============================================

All entrepreneurs agree that building a strong team is extremely important for their startup's success, but many first-time founders are not sure how to achieve it, and are baffled by the interviewing process. The number of questions and choices is indeed confusing: where to get the resumes, whom to invite to an interview, whether to conduct interview over the phone or in person, what to ask, how to evaluate the answers, etc.

Luckily, the structured interviewing approach Will wrote about recently can help. Below are some details of how we apply structured interviewing at Coral8 ( a Silicon Valley startup building a platform for real-time analysis of large volumes of data). While what follows applies mainly to engineers (software, QA, support, professional services), the same would apply to many other job functions and positions.

Like any complex process, the interviewing process is best structured and analyzed as a sequence of phases. At Coral8, we have four phases: email interview, phone interview, the first in-person interview (with 1-2 person), the second in-person interview (3-4 others). Whether you have the same stages or not is not important. What's important is having a clear understanding of a) why you are having each phase b) what you are trying to accomplish, and c) how you are going to evaluate the results. It helps if all the interviewers share this understanding, and keep the process as consistent across candidates as possible.

Let's consider the phases separately.

Email interview

---------------

Most startups complain that just finding a good candidates is the hardest part of the process. Post a job description at any jobs web site, and you'll receive hundreds of resumes, most of them from people who are not even remotely qualified. Hire a recruiter, and he'll be sending dozens of resumes your way, again often from poorly qualified candidates. Just opening and reading those resumes is often overwhelming.

The problem may seem impossible to solve, yet a simple solution exists, and here at

Coral8 we are still puzzled as to why so few companies use it. Here is what you do: You never, ever, publish a position description without an accompanying problem that someone MUST solve before you even open their resume. The problem

should: a) have a solution that can be easily reviewed b) take the right candidate about 10 minutes to complete c) test a skill that is core to the job

d) be somewhat interesting e) allow a super-star candidate to show off their

knowledge and skill. Since most of our positions require programming in some

language, our problems often require writing a simple program or function. The language and the complexity is adjusted for each position.

For example, when we interview C++ engineers, we want to make sure they understand polymorphism and virtual functions. It's disturbing how many people who call themselves C++ programmers do not. So here is a problem we sometimes

use: Illustrate the use of the keyword "virtual" by writing a short C++ program which contains this keyword and prints "Hello, world". If the keyword "virtual"

is removed, the modified program should print "Good bye, world".

Some may say that the problem is too simple, and it certainly is. But having a problem like this in your ad does wonders. First, it greatly raises the signal-to-noise ratio. Few Visual Basic programmers will bother to send their resumes if you require a solution to a C++ problem. If they do, or when the solution is wrong, you can quickly ignore the submission. The resumes you'll get are usually from people who are really motivated, and not just sending resumes to all the positions. If somebody gives you a correct solution, you immediately know that you have a strong candidate.

Some folks may think that having a problem discourages some good candidates from applying for a job. Who knows, maybe this is true for some candidates. In our experience, however, we find just the opposite. Some of the very best employees we've hired told us that they applied for a position with Coral8, back then a stealth-mode startup, precisely because they were intrigued and challenged by our posted problems.

What if you do not publish your job openings, but instead use recruiters? Easy!

Give the problem to the recruiter, and tell him that you will not accept any resumes without the solution to this problem. Some recruiters will tell you they don't want to do the extra work. Somehow these are often the recruiters who want to charge you 25-30% of the candidate's annual salary, and you just pass on them. A startup can and should negotiate a much better deal anyway, and, more important, a good recruiter loves the fact that you have this problem!

Why? They know that you get a lot of resumes, from many sources. They want to give you the candidates who are the most qualified, and they have to qualify them somehow anyway. And what better way is there to qualify the candidates than to use your own problem?

So this is what we call an "email interview". In most cases, unless we have a high-quality referral, we refuse to even look at the resume unless we see a solution to our problem. Life is too short to look at hundreds of resumes a week.

Phone interview

---------------

Phone interviewing is a much more traditional and better understood process, so I won't spend as much time on it. What we found important is to have a list of questions for each position, and to try to follow this list every time. It makes the process much better structured, and over time you learn which questions are harder than you thought, and which ones are easier. So it helps you calibrate your expectations better.

Since we only schedule phone interviews with the people who pass the email interview, we know they have at least some basic understanding of one area. So the phone interview is used to get a slightly better understanding of the breadth and the depth of the candidate's skills. We spend about 30 minutes with a candidate, and use a part of that time telling the candidate about the company and the position. After 30 minutes, it is usually clear if you want to invite the candidate to a face-to-face interview.

1st face-to-face interview

---------------------------

All right, the candidate comes in to see you, what do you do? As Will mentioned, too many interviewers go with "Tell me about yourself?" and "Tell me about your past projects?" kind of questions. These questions are ok, but spending more than 10-15 minutes on them is counter-productive. The last question is often useless, unless you happened to know a lot about specific areas the candidate worked in. If you do not, it's hard to evaluate how challenging the tasks really were, and whether the decisions he made were correct. Instead, what you should evaluate in these situations is the candidate's presentation skills. Whether you are an expert in his area or not, any good candidate should be able to clearly explain to you what he did, what the overall project was, what the trade-offs were, etc.

But most of the time should be spent with the candidates answering a carefully constructed set of questions. This may be a religious issue, but we at Coral8 strongly believe that the questions should be clearly related to the job, and not some puzzles that test nothing but the ability to solve puzzles.

Now, if you are interviewing programmers, then please, please, please, administer some programming exercises. There is an amazing number of programmers on the market with fancy resumes, fancy titles, and fancy degrees from fancy schools, who nevertheless cannot program well. You do not want to hire people like that. Any resistance to programming during the interview (e.g, "I don't program well during interviews") should be an immediate red flag.

Of course, when you ask somebody to code during the interview, be reasonable.

Many people do not remember the language syntax or the names of library functions. That's entirely ok. We either let people use some reference guide or Google, or just tell them that they should not worry syntax. To us, what matters most is algorithms, so this is what we pay attention to. You may worry more about something else, but whatever it is, make sure you carefully construct your questions to test for that, rather than just asking whatever you feel like at the moment.

2nd face-to-face interview

--------------------------

Now, the candidate passed your interview, and you invited him to come again to "meet the team." Sounds innocent, but this is one of the more challenging parts of the process. You've got to recognize that people have widely different interviewing skills, and sometimes even great engineers make poor interviewers.

Work with them. Agree, as a team, on which questions to ask, and who will ask them. Sit in on some interviews yourself, to make sure you are satisfied with the interview dynamics. It's often best if people interview in pairs: it takes less candidate's time and lets the interviewers to learn from each other.

The 2nd face-to-face interview is also a good time to further investigate some

personality issues. For example, the team may agree that during the interview,

one team member will try to push the candidate a bit, disagree with him strongly on some issues, and see how the candidate handles it. You don't want to go too far, but it's a useful test. Nothing kills productivity in a startup like engineers who do not know how to disagree with each other professionally.

All right, everybody has talked to the candidate, now what? This is the place where it's especially important to have a well-defined process. It's best to have a formal scale, on which everybody will grade the candidate. The scale we have at Coral8 was popularized by Siskel and Ebert: thumbs up, thumbs down, and we also have many gradations in between. It's not important what you have, the scale 1-10 works just as well.

It also helps to have a threshold. Let's say your threshold is 7. It means that you do not want to hire anybody with the average score below 7. If you have only one serious candidate for the position, you just need to decide whether he scored above your threshold or not. If you have multiple candidates, you need to compare them to each other, using their combined scores.

How you combine the scores given by different team members is an art, not a science. You may start with simple averaging. Or you may want to say that anybody with one or two votes below the threshold is automatically disqualified.

You may also keep in mind that one person's 9 may well be another person's 6.

The ultimate decision is yours, but what's important is that you as a team talk about the candidate, and discuss what people like and dislike about the person.

During this discussion, you'll learn a lot about the candidate, and you'll learn even more about your team!

Conclusion

----------

There are many parts of the hiring process that we have not covered yet: formal reference check, informal reference check, offer negotiation, etc. The important point, however, may have nothing to do with hiring per se. To many people, the words "startup" and "process" are mutually contradictory. Processes are for Fortune 500 companies, right? Not so fast. Like it or not, there are many processes going on in any startup. You may recognize, structure, and optimize them. Or you may hope that they just work by themselves. The interviewing process is a good example of a process that will produce some results either way: after all, no startups die because they cannot hire any people at all. But there are certainly ways to make this process much more effective, efficient, and enjoyable for all participants.

Monday, June 05, 2006

Wednesday, May 24, 2006

Managing Growth

Today, I had the good fortune of sitting in on a lecture by Verne Harnish on how to increase the value of fast-growth companies. Verne is the author of Mastering the Rockefeller Habits and CEO of Gazelles Inc. My host, a major Internet company, brought Verne in to provide senior and mid-level management a framework and set of best practices for managing growth and creating value. The subject matter is dear to my heart and a critical area of study for any start-up manager.

Verne's book is based on the management style of John D Rockefeller. Rockefeller's management style centered on three key areas: priorities (define the 1-5 most important organizational objectives), data (identify and manage to the key metrics and leading indicators), and rhythm (run a well-organized set of daily, weekly, monthly, and quarterly meetings that keep everyone aligned and accountable). The core premise is that success is the sum total of all decisions being made in an organization. Leaders/managers influence decisions, and hence success, and need a framework regarding how best to do so.

Verne laid out his 4-3-2-1 framework for how great managers can optimize decisions.

Managers have four decision levers:

Often start-ups feel that data-driven management is an oxymoron, that meetings are a waste of time, and that communication by email is the most effective way to get things done in a crazy, fast-paced world.

Verne's rebuttal to that world-view is that relentless repetition and routine frees the company to shine and grow confident that energy and effort are aligned with the end game. He advocates meeting and managing to a few key priorities, daily "talk time" where the team can spend 10-15 minutes reviewing pressing issues, daily data and indicators, and bottlenecks that require resolution creates incredible energy, collaboration, and productivity. He recounted multiple examples of companies that make a daily meeting an essential rhythm of corporate life and benefit in doing so.

As an investor and ex-CEO of a start-up, I relate very well to Verne's approach. Companies need to select a framework and language of dialogue that centers the team on common goals, common metrics, and creates a forum for cross-function collaboration, problem resolution, and productivity. While this is common sense, too often common sense is lost to inertia and productivity grinds to a halt as misalignment and misdirection sap energy, cash, and momentum. Whether Verne's framework or another, picking a methodology to detail priorities, metrics, and company alignment and communication can make implicitly intelligent ideas explicit mechanisms of management and key tenents of company culture.

With respect to growth, he argued that the faster the rhythm (group meetings and metric reviews), the faster you will grow. Seems counter-intuitive that meeting time accelerates productivity - but if a short, stand-up meeting eliminates bottlenecks, realigns priorities and strategy, and enhances cross-team synergy then it is somewhat obvious productivity will be enhanced. This is very similar to the role of the Scrum master in agile development.

His site provides templates for strategic plans, daily and weekly meetings, and other useful materail.

Finally, he left the group with two sets of looming questions.

The first set is what is the business question we need to answer? What is the key problem/question whose answer will free us to grow at 2x the competition, 2x the cashflow, 3-5x the profitability, and 10x the market cap? He also suggests picking a key personal question that will similarly accelerate personal growth and development.

The second question is to determine what to stop doing. What wastes time, is inefficient, gets in the way of true productivity - answer the question and get rid of it.

Thank you to my host and to Verne for a great day and lots of food for thought.

Verne's book is based on the management style of John D Rockefeller. Rockefeller's management style centered on three key areas: priorities (define the 1-5 most important organizational objectives), data (identify and manage to the key metrics and leading indicators), and rhythm (run a well-organized set of daily, weekly, monthly, and quarterly meetings that keep everyone aligned and accountable). The core premise is that success is the sum total of all decisions being made in an organization. Leaders/managers influence decisions, and hence success, and need a framework regarding how best to do so.

Verne laid out his 4-3-2-1 framework for how great managers can optimize decisions.

Managers have four decision levers:

- people (happiness, turnover, applicants/job opening, quality applications/total applicants)

- strategy (revenue/growth)

- execution (profit/time)

- cash

- priorities

- metrics/data

- meeting rhythm

- reputation

- productivity

Often start-ups feel that data-driven management is an oxymoron, that meetings are a waste of time, and that communication by email is the most effective way to get things done in a crazy, fast-paced world.

Verne's rebuttal to that world-view is that relentless repetition and routine frees the company to shine and grow confident that energy and effort are aligned with the end game. He advocates meeting and managing to a few key priorities, daily "talk time" where the team can spend 10-15 minutes reviewing pressing issues, daily data and indicators, and bottlenecks that require resolution creates incredible energy, collaboration, and productivity. He recounted multiple examples of companies that make a daily meeting an essential rhythm of corporate life and benefit in doing so.

As an investor and ex-CEO of a start-up, I relate very well to Verne's approach. Companies need to select a framework and language of dialogue that centers the team on common goals, common metrics, and creates a forum for cross-function collaboration, problem resolution, and productivity. While this is common sense, too often common sense is lost to inertia and productivity grinds to a halt as misalignment and misdirection sap energy, cash, and momentum. Whether Verne's framework or another, picking a methodology to detail priorities, metrics, and company alignment and communication can make implicitly intelligent ideas explicit mechanisms of management and key tenents of company culture.

With respect to growth, he argued that the faster the rhythm (group meetings and metric reviews), the faster you will grow. Seems counter-intuitive that meeting time accelerates productivity - but if a short, stand-up meeting eliminates bottlenecks, realigns priorities and strategy, and enhances cross-team synergy then it is somewhat obvious productivity will be enhanced. This is very similar to the role of the Scrum master in agile development.

His site provides templates for strategic plans, daily and weekly meetings, and other useful materail.

Finally, he left the group with two sets of looming questions.

The first set is what is the business question we need to answer? What is the key problem/question whose answer will free us to grow at 2x the competition, 2x the cashflow, 3-5x the profitability, and 10x the market cap? He also suggests picking a key personal question that will similarly accelerate personal growth and development.

The second question is to determine what to stop doing. What wastes time, is inefficient, gets in the way of true productivity - answer the question and get rid of it.

Thank you to my host and to Verne for a great day and lots of food for thought.

Friday, May 19, 2006

Applied Interviewing

Interviewing candidates is an art and a challenging one. Hiring the best and brightest, establishing competency, qualifying cultural fit, and making interviewing productive are critical to the success of early stage companies. In order to avoid superficial discourse and backing-in to a process that rewards conversational skills rather than material functional skills, it is helpful to train people in structured, applied interviewing.

Too often, people walk into interviews armed with little more than a resume and ask, “so tell me about yourself.” There is an awkward dynamic where the candidate is eager to convey their strengths and the interviewer wants to qualify the “fit” of the applicant. And yet, far too often, the output of the interview is , “I liked them,” or,

“I don’t think they are a fit.”

Given the massive importance of hiring the right people, screening for the right skills, and making the best use of the time consuming interview process it really pays think about how best to evaluate talent. Structured, applied interviewing moves the interview away from conversational skills and the serial recounting of someone’s background to a focus on the specific skills that are relevant to the hire in question.

For each department, I encourage start-up teams to jointly develop a set of questions, case studies, and applied examples of the skills in question. Then train each interviewer in how to best ask the questions and use the structured material. Group evaluations can then center on a common framework and a targeted output. For example, for engineers the interview could center of logic and coding tests, for VP sales on forecasting methodologies, CRM systems of choice, pipeline and sales force management…In my case here at Hummer Winblad, the team asked me to present my thoughts on the future of the software industry, in a one hour presentation, to the full partnership. My ability to present, articulate a thesis, and provide a framework for analysis were made transparent and the final evaluation allowed for skills and cultural fit to be taken into account.

After interview-day dinners can help with the cultural fit questions, however, for the scheduled interviews I suggest avoiding the conversational approach for a vetted, structured approach that helps make the interviewing process more productive in terms of both time and results.

People, after all, are the most input into any growing business.

Thursday, May 18, 2006

SVASE - VC Breakfast

Next Thursday, I will be involved in a SVASE VC breakfast event. The event is Thursday, May 25th at 8am at 50 Fremont St in San Francisco.

Per the SVASE site:

Per the SVASE site:

"The VC Breakfast club provides an intimate setting and meeting place for one VC and up to ten entrepreneurs who meet for breakfast every week. The participating VC listens to each entrepreneur's extended elevator pitch and provides immediate feedback - enabling fast, effective, accessible mentoring and relationship development."

I look forward to meeting some great entrepreneurs.

Wednesday, May 17, 2006

Cash Breakeven Analysis

In the spirit of sharing best practices in start-up management, I write to share some interesting analysis on cash breakeven forecasting that I saw at a recent BOD meeting. The BOD deck included a simple yet powerful slide that helps understand the size of the "cash gap" derived from analyzing the make-up of monthly cash expenses, current monthly recurring cash revenue base, and average monthly sales price. Simply graph total montly cash expenses by category vs existing recurring monthly revenue - illustrate the size of the gap and note how many incremental sales * contribution margin it will take to close the gap.

An example is below:

Tuesday, May 09, 2006

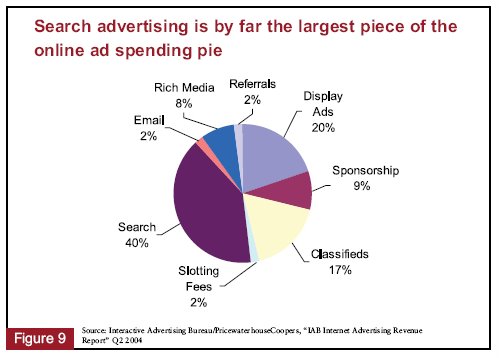

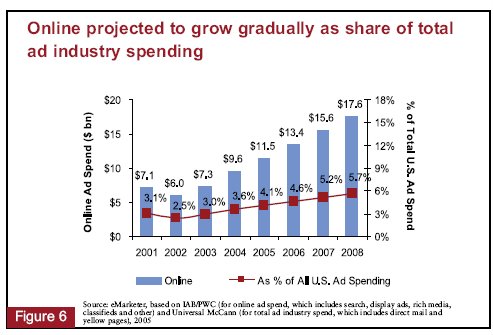

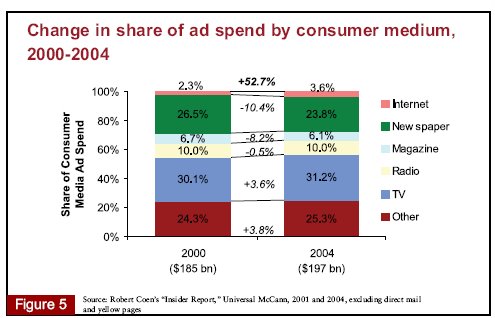

Follow the User

In 2006, American industry will spend $290 bn on advertising. How much will be spent on-line as a percentage of the total? 4.6%, or $13.4bn.

It is quite remarkable that despite the pay-for-performance advantages and closed-loop nature of on-line spend versus off-line spend that the number is so low. Newspaper spend is 6.6x that of on-line spend - why? How long can this last?

In many ways, on-line ad spending is changing our relationship to our service providers - more and more content and application functionality is ad-supported - email, storage, video, news, calendaring, IM, 411 calls, etc - and the companies that recognize the move to providing users high-quality product while providing advertisers high-quality demographics and targeting mechanisms are clearly winning.

Google's model: revenue = users x queries/user x ads/query x clicks/ads x revenue/click is powerful. Queries provide targeting information (what is someone looking for, watching, blogging about), clicks provide insight and accountability (how many consumers find this campaign relevant and useful), and revenue/click helps advertisers understand cost of customer acquisition and helps site that provide meaningful user populations, user segmentation and targeting monetize their users.

Questions to Ask

Quick post sharing some of my favorite questions to ask entrepreneurs thinking through enterprise business plans and strategies....the questions help me think through the merits of enterprise software start-up strategies given today's IT environment.

What is the time to value quotient? How long does it take for the customer to realize value from your product? Compare and contrast clicking on a URL to self-provision versus a two-month on-premise proof of concept.

What is the customization to value quotient? How much customization is required before the customer sees relevance and value?

How much manual labor is required to realize value? How many sales engineering and professional services hours are required to both explain the merits of the solution and have it running successfully in the customer's environment? The common element of MySQL or Salesforce.com appears to be that customers self-validate through low-risk experimentation without the need for vendor sales engineers.

What is the risk of experimentation? Does the customer need to pay for a proof of concept? Does the customer need to requisition IT resource (new servers, open up a firewall port, etc) to enable your product to showcase its benefit? As with the MySQL comment above, can the customer experiment and test the value proposition without material risk or expense?

What is the time to integration? Can the product provide standalone value that obviates the need for day one systems integration, a la SFA? To the extent integration is required, how standardized are the interfaces to relevant up and downstream systems that add value to the solution?

The consumer internet offers useful lessons and direction for the enterprise space. Customers self-provision, self-validate, self-integrate, and self-configure.

What is the time to value quotient? How long does it take for the customer to realize value from your product? Compare and contrast clicking on a URL to self-provision versus a two-month on-premise proof of concept.

What is the customization to value quotient? How much customization is required before the customer sees relevance and value?

How much manual labor is required to realize value? How many sales engineering and professional services hours are required to both explain the merits of the solution and have it running successfully in the customer's environment? The common element of MySQL or Salesforce.com appears to be that customers self-validate through low-risk experimentation without the need for vendor sales engineers.

What is the risk of experimentation? Does the customer need to pay for a proof of concept? Does the customer need to requisition IT resource (new servers, open up a firewall port, etc) to enable your product to showcase its benefit? As with the MySQL comment above, can the customer experiment and test the value proposition without material risk or expense?

What is the time to integration? Can the product provide standalone value that obviates the need for day one systems integration, a la SFA? To the extent integration is required, how standardized are the interfaces to relevant up and downstream systems that add value to the solution?

The consumer internet offers useful lessons and direction for the enterprise space. Customers self-provision, self-validate, self-integrate, and self-configure.

Friday, April 28, 2006

Business Plan Dependencies

In designing a business plan, it pays to ask, "what are the business plans' dependencies on variables beyond the company's control?" Why? Because the probability of success is inversely proportional to the number of exogenous variables.

Let's assume the business is dependent on five market factors materializing and each independent variable has a 50% chance of occurring - the odds of failure are then 1-(.5^5), or 96.875%. Not good. The odds of start-up success are already daunting; making the odds even more daunting by attempting to execute a plan overly dependent on external variables is a recipe for frustration.

What do I mean? Well, if a business plan requires

Let's assume the business is dependent on five market factors materializing and each independent variable has a 50% chance of occurring - the odds of failure are then 1-(.5^5), or 96.875%. Not good. The odds of start-up success are already daunting; making the odds even more daunting by attempting to execute a plan overly dependent on external variables is a recipe for frustration.

What do I mean? Well, if a business plan requires

- distribution deals to reach the end-market (ex. wireless carriers)

- deployment of new networks, infrastructure, and network devices (ex. wimax, rfid readers)

- new device proliferation (ex. Windows Mobile only)

- new technology (broadband over powerline)

- etc...

Thursday, April 27, 2006

America's Competitiveness

Today, the NVCA announced Magnet USA, a program designed to strengthen America's competitive position in the global economy. I am all for programs designed to stimulate and encourage innovation. Innovation creates jobs, wealth, and increased social utility. However, America's long term security and capacity to support innovation is under tremendous pressure.

Bill Gross' recent column compares the future fate of America to the current state of GM. Gross attributes GM's malaise to uncompetitive labor costs and the burden of pension and health care liabilities. He argues that we are glimpsing America's future in the GM's current struggle to remain solvent, reduce its fixed costs, and reduce future pension and healthcare obligations via employee buyouts. It is a worthwhile and scary read.

Is this overly negative thinking? I went to Whitehouse.gov and read through the OMB's assessment of America's future to find out. Unhappily, I found the following:

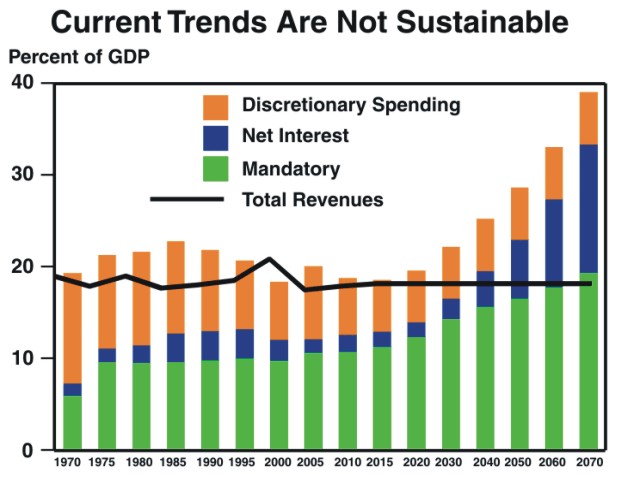

"While the near-term outlook for shrinking deficits is encouraging, the long-term picture presents a major challenge due to the expected growth in spending for major entitlement programs. In only two years, the leading edge of the baby boom generation will become eligible for early retirement under Social Security. In five years, these retirees will be eligible for Medicare. The budgetary effects of these milestones will be muted at first. But if we do not take action soon to reform both Social Security and Medicare, the coming demographic bulge will drive Federal spending to unprecedented levels and threaten the NationÂ’s future prosperity.

No plausible amount of cuts to discretionary programs or tax increases can help us avert this major fiscal challenge. As the accompanying chart shows, assuming mandatory spending continues on its current trajectory and the tax burden is held at historical levels, by 2040 Federal spending will accelerate to a level at which mandatory outlays and debt service would consume all Federal revenue. By 2070, if we do not reform entitlement programs to slow their growth, the rate of taxation on the overall economy would need to be more than doubled, placing a crushing burden on the economy that is required to produce the revenues to support the Government programs in the first place."

Wow. According to the OMB, by 2040 all our tax revenue will go to entitlement spending and debt service. How we will invest in the future - research, education, infrastructure - if we are seeing an ever smaller amount of US government revenues available for discretionary spending?

The technology market feels good right now - new companies, models, and innovation is strong. What frightens me is when the OMB and major bond holders forecast a financial meltdown and the eventual devaluation of the US currency, rising interest rates, and a social contract (entitlement spending) that will literally break the bank.

As the VC industry discusses globalization and the merits of offshore investing, a key part of the conversation may be the fundamental, long term macro trends that are shaping the face of future opportunity and innovation. Certainly, the OMB paints a bearish view of America and a compelling reason to start thinking about offshore investing and non-US dollar holdings.

I recently heard someone argue that capital is a coward - it seeks refuge in safe-havens. Unless, we in America are able to make difficult decisions and reduce the fixed costs in the governmemt budget, as GM is laboring to do today, capital will eventually flow out the US and to more attractive safe harbors. Hopefully, unlike energy policy/problems, these entitlement burdens will become part of the political discourse while we still have time to make painful choices to avert painful outcomes.

Tuesday, April 18, 2006

Concept to Company Update - Great Event

Tonight, VLAB and Hummer Winblad hosted a wonderful panel at Stanford Business School titled Concept to Company: Strategies for Swimming with the Sharks.

This year's Concept-to-Company event focused on the business formation of Cittio, a network management software company founded in 2001 and funded by Hummer Winblad last year. Ann Winblad moderated the panel, Jamie Lerner, Cittio's CEO served as the keynote speaker, and the panelists included Sandeep Johri, Oblix's founding CEO and currently HP Software's VP Strategy and Business Planning, Deborah Magid, IBM Software's Director of Strategy, and Elisabeth Rainge, IDC's Network Management analyst.

The evening's conversation centered on how start-ups best can enter mature markets dominated by incumbents. Network management is a $5+bn software market owned by IBM, HP, BMC, and CA. Jamie set out to answer how best to archetype an offering innovation, sales and delivery model, and marketing message that resonates with buyers in a market long controlled by larger vendors.

Jamie's advice centered on when to raise VC money, how to pick your VC partner, how to pitch VCs, how to sell against giants, and how to handle incumbents' FUD.

When To Raise VC Money

Jamie believes in bootstrapping companies. While I believe this is not a requirement, Jamie believes start-ups are best served by eliminating key market, customer, and product risks prior to soliciting venture firms. Jamie calls his strategy the "just add water approach;" walk in to meetings having validated a big market, shipped a solid product, sold paying customers, operated a well managed business, and hired a good team. He believes entrepreneurs should validate the following five hypotheses:

How to Pitch VCs

Jamie suggested the following structure for good pitches:

This year's Concept-to-Company event focused on the business formation of Cittio, a network management software company founded in 2001 and funded by Hummer Winblad last year. Ann Winblad moderated the panel, Jamie Lerner, Cittio's CEO served as the keynote speaker, and the panelists included Sandeep Johri, Oblix's founding CEO and currently HP Software's VP Strategy and Business Planning, Deborah Magid, IBM Software's Director of Strategy, and Elisabeth Rainge, IDC's Network Management analyst.

The evening's conversation centered on how start-ups best can enter mature markets dominated by incumbents. Network management is a $5+bn software market owned by IBM, HP, BMC, and CA. Jamie set out to answer how best to archetype an offering innovation, sales and delivery model, and marketing message that resonates with buyers in a market long controlled by larger vendors.

Jamie's advice centered on when to raise VC money, how to pick your VC partner, how to pitch VCs, how to sell against giants, and how to handle incumbents' FUD.

When To Raise VC Money

Jamie believes in bootstrapping companies. While I believe this is not a requirement, Jamie believes start-ups are best served by eliminating key market, customer, and product risks prior to soliciting venture firms. Jamie calls his strategy the "just add water approach;" walk in to meetings having validated a big market, shipped a solid product, sold paying customers, operated a well managed business, and hired a good team. He believes entrepreneurs should validate the following five hypotheses:

- Demand - select a large, established market to operate in and prove the innovation

- Product - develop a complete and working product

- Customers - referenceable accounts, good logos, and revenues

- Profitability - prove efficiency, discipline, and frugality

- Team - key players in place to grow

How to Pitch VCs

Jamie suggested the following structure for good pitches:

- 10 slides

- be crisp, clear, and articulate about the market need, offering innovation, and sales and delivery model

- 5 year GAAP pro formas